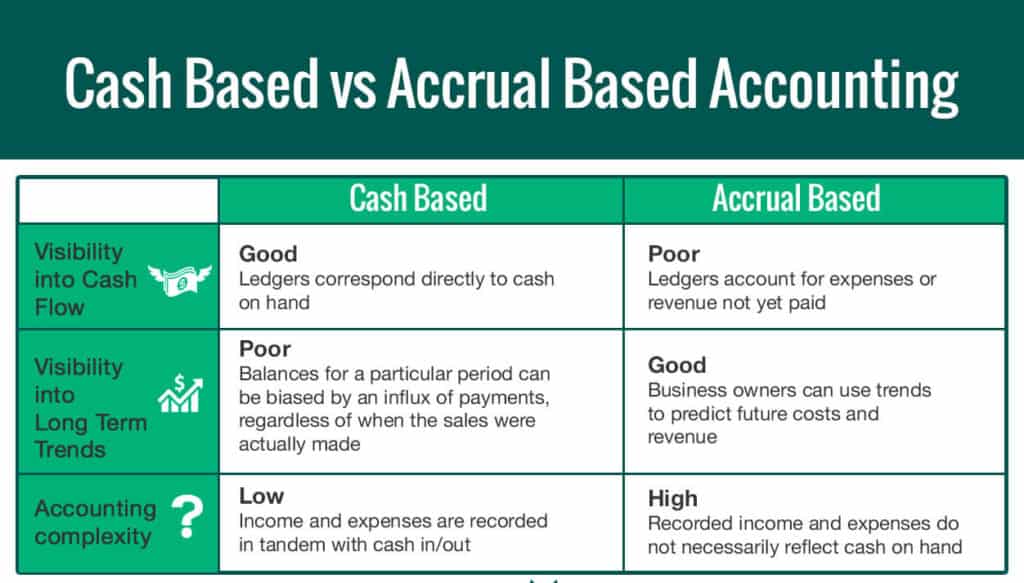

Investors would then be left in the dark as to the actual sales performance and total inventory on hand. Accrual basis accounting requires companies to recognize revenue when it’s earned. The term earned generally means when a product is delivered Why is the accrual basis of accounting generally preferred or a service is completed. Incurred refers to when a cost is paid in cash or when a liability is created (accounts payable, for example). The accrual basis recognizes revenue and expense without regard to cash inflows and outflows.

Accruals are a key part cash basis of the closing process used to create financial statements under the accrual basis of accounting; without accruals, financial statements are considerably less accurate. It reflects a better association of revenues and expenses with the appropriate accounting period. The accrual basis of accounting recognizes all resource changes when they occur. The cash basis of accounting limits the recognition of resource changes to cash flows.

Accounting Concepts

While the accrual basis of accounting provides a better long-term view of your finances, the cash method gives you a better picture of the funds in your bank account. This is because the accrual method accounts for money that’s yet to come in. With the accrual accounting method, income and expenses are recorded when they’re http://www.elenorjaneevents.co.uk/?p=242573 billed and earned, regardless of when the money is actually received. Accrual basis accounting more completely reports both financial performance and position. It is generally preferred by accountants, because it shows when revenue has been earned and debts incurred, regardless of whether money has yet changed hands.

Difference Between Cash And Accrual Accounting

The downside of this method is that you pay income taxes on revenue before you’ve actually received it. Additionally, if you are planning Why is the accrual basis of accounting generally preferred to sell your business, potential buyers will also want to see GAAP-compliant financial statements that use accrual basis accounting.

The sale is entered into the books when the invoice is generated rather than when the cash is collected. Likewise, an expense occurs when materials are ordered or when a workday has been logged in by an employee, not when the check is actually written.

An important decision for any business is whether to adopt accrual or cash basis accounting. In very simple terms, accrual basis accounting https://simple-accounting.org/ records income when earned and expenses when incurred, whether or not accompanying receipts and payments happen at the same time.

The January income statement will report the collection of the fees earned in December, and the February income statement will report the expense of using the December utilities. Hence, the cash basis of accounting can be misleading to the readers of the financial statements. The cash basis Why is the accrual basis of accounting generally preferred of accounting recognizes revenues when cash is received, and expenses when they are paid. Cash basis is a major accounting method by which revenues and expenses are only acknowledged when the payment occurs. Cash basis accounting is less accurate than accrual accounting in the short term.

Meanwhile, the advantage of the accrual method is that it includes accounts receivables and payables and, as a result, is a more accurate picture of the profitability of a company, particularly in the long term. The reason for this is that the accrual method records all revenues when they are earned and all expenses when they are incurred. The cash method is mostly used by small businesses and for personal finances. Accrual accounting means revenue and expenses are recognized and recorded when they occur, while cash basis accounting means these line items aren’t documented until cash exchanges hands.

Penalties On Self Employment Tax

Most businesses are paid after they actually deliver products or services, and they often pay for goods and services after receiving them. Both processes frequently cause the actual cash settlement to occur in a different period than when the obligations occurred. Let’s assume that I begin an accounting business in December and during December I provided $10,000 of accounting services. Since I allow clients to pay in 30 days, none of the $10,000 of fees that I earned in December were received in December.

- Without the periodicity assumption, a business would have only one time period running from its inception to its termination.

- Previously, we demonstrated that financial statements more accurately reflect the financial status and operations of a company when prepared under the accrual basis rather than the cash basis of accounting.

- The periodicity assumption requires preparing adjusting entries under the accrual basis.

Comparing Accrual Basis To Cash Basis

That way, recording income can be put off until the next tax year, while expenses are counted right away. Accrual accounting is a method of accounting where revenues and expenses are recorded when they are earned, regardless of when the money is actually received or paid. For example, you would record revenue when a project is complete, rather than when you get paid. In the next month, the entry reverses, creating a negative $20,000 expense that is offset by the arrival and recordation of the supplier invoice.

Previously, we demonstrated that financial statements more accurately reflect the financial status and operations of a company when prepared under the accrual basis rather than the cash basis of accounting. The periodicity assumption requires preparing adjusting Why is the accrual basis of accounting generally preferred entries under the accrual basis. Without the periodicity assumption, a business would have only one time period running from its inception to its termination. Accrual basis accounting is the standard approach to recording transactions for all larger businesses.

This month XYZ placed an order for $8000 worth of materials, and received a payment of $12,000 for its last batch of widgets sold. Any business owner knows that you don’t pay your bills with “revenue.” You pay them with cash, so cash flow is just as important to companies using accrual accounting as cash accounting. That’s why GAAP calls for a business to produce regular cash flow statements, which track cash coming into and out of the business, separate from the revenue and expenses that get booked on the income statement. Combined, the income and cash flow statements present a full picture of when the company earns its money and when it gets its money.

Analyzing Accrual Accounting

The accrual method is most commonly used by companies, particularly publicly-traded companies. For example, under the cash method, retailers would look extremely profitable in Q4 as consumers buy for the holiday season but would look unprofitable in Q1 as consumer spending declines following the holiday rush. One of the main ways to assess the efficiency of a company’s accrual accounting is to survey the accrual accounting impact across all of the company’s financial statements.

Cons Of Cash-basis Accounting

Because the cash basis of accounting does not match expenses incurred and revenues earned in the appropriate year, it does not follow Generally Accepted Accounting Principles (GAAP). The cash basis is acceptable in practice only under those circumstances when it approximates the results that a company could obtain under the accrual basis of accounting.

Definition Of The Cash Basis Of Accounting

The accrual basis of accounting also allows you to expense large items that cover several months and the business pays in arrears, such as real estate tax. Under the accrual method, transactions are counted when the order is made, the item is delivered, or the services occur, regardless of when the money for them (receivables) is actually received or paid.

Virtually all lenders and investors will want to see financial statements prepared in accordance with GAAP before extending financing or pledging equity capital. Therefore, if your bookkeeper or CPA advises you to use (or continue to use) cash accounting, he or she is not looking out for your best interests — and you should strongly consider a change. An outsourced CFO services provider who is experienced in financial statement preparation can provide training and instruction to your financial and accounting staff in the nuances of accrual accounting. Using the cash basis of accounting the December income statement will report $0 revenues and expenses of $1,500 for a net loss of $8,500 even though I had earned $10,000 in accounting fees. Further, the balance sheet will not report the obligation for the utilities that were used.

Recent Comments